Table of contents

- What Is Stripe Link's Agent Wallet and Why It Matters Now

- How Stripe Link Works for AI Agents

- How Users First Encounter Stripe Link

- Stripe Link and AI Agents: ChatGPT, Perplexity, and Other Platforms

- You Stay in Control: The Approval and Security Model

- Practical Use Cases: Where Agent Wallets Change the Game

- What This Means for Sellers and Platforms Building on Stripe

- How to Get Started with Link Agent Wallets Today

- What's Coming Next: The Roadmap for Agentic Payments

- Frequently Asked Questions

- Putting It All Together

Stripe + Link Agentic Payment Solution: What Founders and Marketers Need to Know

AI agents are no longer just answering questions or drafting emails. They are starting to buy things. And the infrastructure to support that shift just got a major upgrade.

At Stripe Sessions 2026, Stripe announced the Link agent wallet, a product that lets AI agents spend money on your behalf without ever seeing your real payment credentials. You stay in control. You approve every purchase. And the whole thing runs on Stripe's existing payments infrastructure.

This is not a small product update. It is a foundational shift in how commerce works when AI is in the loop. If you are a founder building a product, a marketer managing tools and subscriptions, or a platform operator thinking about where commerce is heading, this article will walk you through exactly what was launched, how it works, and what it means for your business.

What Is Stripe Link's Agent Wallet and Why It Matters Now

Stripe has spent years building Link as an accelerated checkout product. The idea was simple: save your payment details once, and check out faster everywhere Link is accepted. The agent wallet takes that same foundation and extends it into a new paradigm entirely.

At Sessions 2026, Stripe framed its broader mission around three pillars: making Stripe more programmable, protecting and propelling businesses with the strength of the Stripe network, and building economic infrastructure for AI. The Link agent wallet sits squarely in that third pillar.

The core promise is this: you can authorize an AI agent to spend money on your behalf, and your actual payment credentials are never exposed to the agent or the merchant. The agent gets access to a controlled payment mechanism. You get a notification when it wants to buy something. You approve or decline. That is the whole loop.

This matters now because the timing aligns with a broader shift in how people are using AI tools. Agents built on models like Claude or custom frameworks are increasingly being asked to complete tasks that involve real-world transactions. Booking travel. Renewing software. Reordering supplies. Until now, the payment step in those workflows required a human to manually enter card details or hand over credentials in an insecure way. The Link agent wallet closes that gap.

Currently, the product is available in the US only, with a global rollout planned. You can join the waitlist at link.com/in/agents. The fact that Stripe is positioning this as a core strategic pillar rather than an experimental side project signals that agentic commerce is where a significant portion of online transactions are heading.

For founders and marketers, the question is not whether this matters. It is how quickly you need to start thinking about it.

How Stripe Link Works for AI Agents

The mechanics of the Link agent wallet are straightforward once you understand the flow. You do not need to be a developer to follow this, though developers will find the implementation details accessible too.

Step one: point your agent to the skill.md file.

Stripe and Link provide a skill.md file that tells your AI agent how to interact with the Link payment system. You point your agent to this file, and it learns the protocol for initiating payment requests. This works with Claude, OpenClaw, and custom-built agents. The open implementation is also available on GitHub for developers who want to inspect or extend it.

Step two: authenticate and grant access.

You authenticate through the Link app and explicitly grant the agent permission to spend on your behalf. This is not a passive opt-in. You are actively authorizing a specific agent to use the payment infrastructure you control.

Step three: the agent makes a purchase request.

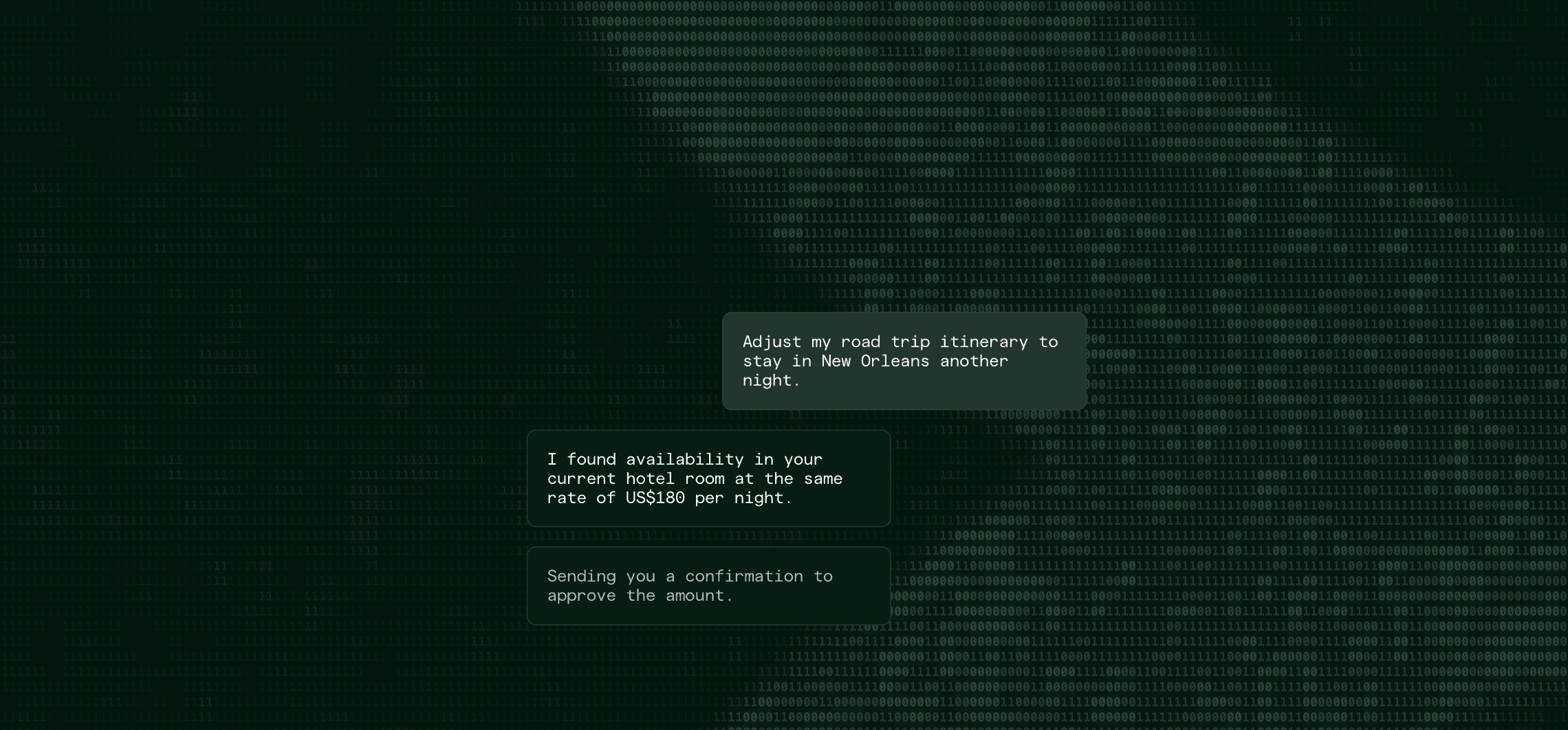

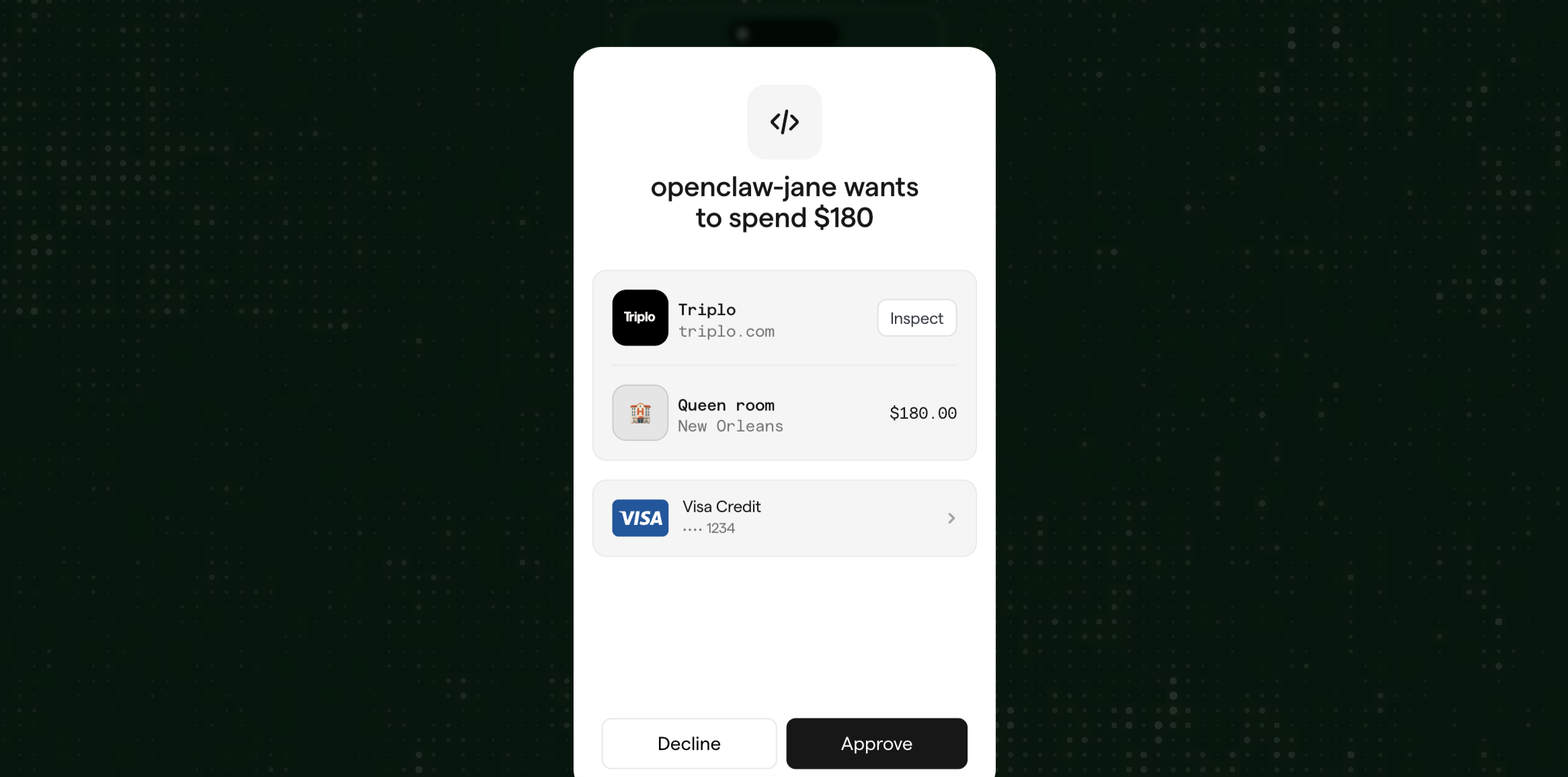

When your agent identifies something it needs to buy, it does not use your real card. Instead, it uses one-time-use virtual cards or shared payment tokens. These are generated specifically for that transaction and are not reusable. Your actual card number, billing address, and credentials stay entirely within the Link system.

Step four: you receive a real-time notification.

Before any money moves, you get an alert in the Link app. The notification shows you the agent name, the merchant, and the amount. For example, you might see: "openclaw-jane wants to spend $180 at Triplo." You tap Approve or Decline. If you approve, the transaction completes. If you decline, nothing happens.

Step five: everything is logged.

Every transaction is recorded in the Link app with the agent name, merchant, amount, date, and approval status. You have a full audit trail of everything your agent has bought on your behalf.

This flow is designed to be low-friction for the user while maintaining meaningful control. The approval step is a single tap, not a multi-step verification process. But it is still an explicit human decision before money moves.

The fact that this works with Claude and OpenClaw out of the box is significant. These are among the most widely used agent frameworks right now. Custom agent support means that teams building proprietary AI workflows can also plug into this infrastructure without waiting for a specific integration to be built.

How Users First Encounter Stripe Link

A common question is how Stripe Link enters someone's life in the first place. The answer depends on whether you are a buyer, a seller, or a developer building on top of Stripe.

For buyers, the most common first encounter is at checkout on a Stripe-powered merchant site. When you complete a purchase, Link may offer to save your payment details for faster checkout in the future. If you opt in, your card is stored in the Link system and becomes available at any other merchant that accepts Link. You do not need to create a separate Link account upfront. The enrollment happens naturally at the point of purchase.

For buyers using AI agents, the first encounter with the agent wallet version of Link is different. You would typically see it when an AI agent you are using surfaces a purchase recommendation and prompts you to connect a payment method. The agent directs you to authenticate through the Link app, where you grant it spending permission. From that point forward, the agent can initiate purchase requests that route through your Link wallet.

For sellers and developers, the first encounter is usually through Stripe's documentation or dashboard. Link is available as part of Stripe's standard checkout and payment element integrations. Enabling it for your checkout does not require a separate contract or a new Stripe account. It is a configuration option within your existing Stripe setup.

Understanding this entry point matters for founders and marketers because it shapes how you think about adoption. Link's network effect grows every time a buyer saves their details at a new merchant. The agent wallet extends that network into AI-mediated commerce, where the buyer may never visit a traditional checkout page at all.

Stripe Link and AI Agents: ChatGPT, Perplexity, and Other Platforms

One of the more specific questions surfacing in search is how Stripe Link connects to AI platforms like ChatGPT and Perplexity. This is worth addressing directly because the answer reveals how the agentic commerce ecosystem is being assembled.

The general model

Stripe is not building a single integration with one AI platform. Instead, it is publishing open protocols, specifically the skill.md file format and the Agentic Commerce Protocol, that any AI agent or platform can implement. This means that an agent running inside ChatGPT, Perplexity, Claude, or a custom-built tool can all interact with the Link payment system using the same underlying mechanism, provided the platform has implemented the protocol.

What this means for ChatGPT

OpenAI has been building out tool-use and action capabilities in ChatGPT. If a ChatGPT-based agent is configured to use the Link skill, it can initiate purchase requests through the same flow described above. The agent surfaces a recommendation, sends a payment request to Link, and the user approves it in the Link app. The ChatGPT interface itself does not handle the payment. Link does.

What this means for Perplexity

Perplexity has been expanding its commerce capabilities, including features that let users buy products directly from search results. The combination of Perplexity's product discovery layer and Stripe Link's payment execution layer is a natural fit. A user could find a product through Perplexity's AI search, and if the merchant is connected to Stripe and the user has a Link wallet, the purchase could complete without leaving the Perplexity interface. Whether Perplexity has formally integrated the Link agent wallet protocol is not publicly confirmed at the time of writing, but the technical pathway exists.

The broader pattern

The pattern here is that Stripe is positioning Link as the payment rail that sits underneath AI-native commerce experiences, regardless of which AI platform the buyer is using. The AI platform handles discovery and recommendation. Link handles payment execution and credential security. This separation of concerns is what makes the open protocol approach viable across a fragmented AI platform landscape.

For founders building on top of AI platforms, this means you do not need to wait for your specific platform to build a native payment integration. If you implement the Link skill in your agent, the payment capability travels with the agent wherever it runs.

You Stay in Control: The Approval and Security Model

The most common concern founders and marketers will have when they hear "let an AI agent spend money on your behalf" is obvious: what stops it from going rogue? What happens if a token is intercepted? Who is liable if something goes wrong?

Stripe and Link have built the security model around a few clear principles.

Your credentials are never shared.

Your actual payment credentials, meaning your real card number, CVV, billing details, are never transmitted to the agent or the merchant. The agent only ever interacts with the virtual card or payment token that Link generates for that specific transaction. This is a meaningful security boundary. Even if an agent is compromised or a merchant's system is breached, your real payment information is not in the blast radius.

Every purchase requires explicit approval.

There is no setting where an agent can spend freely without your knowledge. Every transaction triggers a real-time notification in the Link app, and you must approve it before it goes through. This is not a background process. It is a deliberate design choice to keep humans in the loop at the point of financial commitment.

One-time-use cards limit exposure.

Even if a payment token were somehow intercepted in transit, it cannot be reused. One-time-use virtual cards are generated per transaction and expire immediately after use. This is the same principle behind tokenization in Apple Pay and Google Pay, applied to the agentic context.

Granular controls are coming.

The current version requires approval for every transaction. The roadmap includes granular agent controls that will let you set spending thresholds and pre-approved merchant categories. This means you will eventually be able to say "this agent can spend up to $50 at any SaaS vendor without asking me first" while still requiring approval for anything outside those parameters. That level of control will make the product significantly more useful for recurring or low-stakes purchases.

Full purchase history for auditing.

Every transaction your agent makes is logged with the agent name, merchant, amount, and approval status. If you ever need to review what an agent has been buying, the history is there. This is particularly important for business use cases where expense tracking and accountability matter.

For founders thinking about trust and liability, this model is meaningfully different from giving an agent your card number or using a shared team card. The approval layer and the credential isolation together create a security posture that is actually stronger than most current workarounds people use to let assistants handle purchases.

Practical Use Cases: Where Agent Wallets Change the Game

Abstract infrastructure is only useful when you can see it solving real problems. Here are the scenarios where the Link agent wallet creates genuine value for founders and marketers.

Travel booking

This is the example Stripe and Link use in their own product documentation. An agent finds a hotel room, say a $180 Queen room in New Orleans, and surfaces it to you. Instead of being redirected to a booking site to enter your card details, you get a notification: "openclaw-jane wants to spend $180 at Triplo." You tap Approve. The booking is confirmed. You never left the conversation.

For frequent travelers or teams managing travel logistics, this removes a significant amount of friction from a workflow that currently involves multiple tabs, form fills, and manual credential entry.

SaaS procurement

Marketing and ops teams manage dozens of software subscriptions. Renewals, upgrades, and new tool purchases often require someone to dig up a card, find the right plan, and complete a checkout flow. An agent can handle the research and initiate the purchase. You approve the spend. The subscription is active.

This is particularly useful for teams where the person who evaluates tools is not the same person who has the company card. The agent can do the legwork, surface the recommendation with a price, and route the approval to whoever needs to sign off.

E-commerce reordering

For businesses that regularly restock physical supplies, an agent can monitor inventory signals and trigger reorder requests when stock falls below a threshold. The agent identifies the supplier, confirms the price, and sends you an approval request. You tap yes. The order is placed.

This removes the manual monitoring and checkout steps from a workflow that is currently either fully manual or requires custom automation built on top of supplier APIs.

AI-powered personal shopping

This is the consumer-facing version of the use case. An agent browses products, compares options, and presents a recommendation inside a chat interface. You approve the purchase without being redirected to an external site. The entire shopping experience, from discovery to checkout, happens in the conversation.

For marketers, this is worth paying attention to because it changes where purchase decisions happen. If buyers are completing transactions inside AI chat interfaces, the traditional e-commerce funnel looks very different.

B2B workflows

Finance and ops teams running automated pipelines can use agent wallets to execute approved vendor payments as part of larger workflows. An agent handling invoice processing, for example, could identify a payment that needs to go out, surface it for approval, and complete the transaction once authorized. This is not replacing accounts payable software, but it is adding a payment execution layer to AI-driven workflows that currently stop short of actually moving money.

Each of these use cases shares a common structure: the agent does the research and initiates the request, the human approves the financial commitment, and the transaction completes without credential exposure. That structure is what makes the product genuinely useful rather than just technically interesting.

What This Means for Sellers and Platforms Building on Stripe

The buyer side of the Link agent wallet is the more visible part of the launch. But the seller and platform side is where the long-term infrastructure implications become clear.

Sellers can expose their catalog to agents.

Stripe's agentic commerce documentation describes a model where sellers share their product catalog with AI agents via Stripe's catalog feed and the Universal Commerce Protocol. This means that if you are selling products or services, you can make them discoverable and purchasable by agents acting on behalf of buyers. You do not need to build a custom integration for every agent framework. You publish your catalog in a format agents understand, and Stripe handles the rest.

Platforms using Stripe Connect can enable connected accounts to sell through agents.

For platform operators, the Stripe documentation on enabling in-context shopping outlines a specific integration path. Your platform uploads product feed data and configures checkout hooks for tax and fees. Connected accounts opt in to agent channels. When a buyer makes a purchase through an agent, Stripe runs checkout and calls your platform's hooks before completing the transaction.

This means the platform handles the business logic it already handles, and Stripe handles the agent-facing checkout layer. The integration burden on sellers is significantly reduced because the platform absorbs the complexity.

In-context shopping changes the discovery model.

The phrase "in-context shopping" appears throughout Stripe's agentic commerce documentation, and it describes something that has significant implications for how buyers find and purchase products. Instead of a buyer leaving a conversation to visit a product page, the agent surfaces the product, handles the recommendation, and completes the checkout inside the chat interface. The buyer never navigates away.

For sellers, this means that being discoverable by agents becomes as important as being discoverable by search engines. The catalog feed and Universal Commerce Protocol are the mechanisms through which that discoverability works.

Agentic commerce for platforms is in private preview.

It is worth being clear about where this is in the product lifecycle. Agentic commerce for platforms is currently in private preview and requires waitlist approval in the US. If you are building a platform on Stripe Connect and want to explore this, the path is to go to the Agentic Commerce settings page in the Stripe Dashboard and begin the onboarding process. The onboarding wizard guides you through creating a Stripe Profile, choosing your charge type, enabling agent channels, and configuring seller settings.

For founders building platforms, the private preview status means now is the right time to get on the waitlist rather than wait for general availability. Early access to infrastructure like this tends to create meaningful competitive advantages.

How to Get Started with Link Agent Wallets Today

If you want to explore or implement the Link agent wallet for your business or product, here are the concrete next steps.

For buyers and individuals:

- Join the waitlist at link.com/in/agents. The product is currently US only, with global availability coming.

- Once you have access, point your AI agent to the

skill.mdfile provided by Link. This file tells your agent how to interact with the Link payment system. - Authenticate through the Link app and grant access to the agents you want to authorize.

- Configure which agents are permitted to spend on your behalf. At launch, every transaction requires your approval, so the risk of misconfiguration is low.

The product works with Claude, OpenClaw, and custom-built agents. If you are using a different agent framework, the open implementation on GitHub provides the technical details needed to build a compatible integration.

For platforms and sellers:

- Visit the Agentic Commerce settings page in your Stripe Dashboard.

- Complete the onboarding wizard, which covers creating a Stripe Profile, selecting your charge type, enabling agent channels, and configuring seller settings including webhook endpoints and support policies.

- Upload your product feed data in the format Stripe's catalog feed expects.

- Configure checkout hooks for tax and fee logic.

- Enable connected accounts to opt in to agent channels.

Because agentic commerce for platforms is in private preview, you will need waitlist approval before you can complete this setup. The earlier you apply, the better positioned you will be when access opens up.

For developers:

The open implementation is available on GitHub and supports integration with Claude, OpenClaw, and custom agent frameworks. Stripe's agentic commerce documentation covers the technical concepts including shared payment tokens, catalog feeds, the Universal Commerce Protocol, and the Agentic Commerce Protocol. These are the building blocks for anyone who wants to go deeper than the out-of-the-box integrations.

If you are evaluating whether this infrastructure fits your product, the TryReadable guide library has additional context on how AI-driven commerce tools are changing the way buyers and sellers interact online. And if you want to talk through how agentic commerce might apply to your specific business model, booking a demo is a good starting point.

What's Coming Next: The Roadmap for Agentic Payments

The current version of the Link agent wallet is a strong foundation, but Stripe has been explicit about what is coming next. Understanding the roadmap helps founders plan ahead rather than react after the fact.

Granular agent controls

The most immediately useful upcoming feature is granular agent controls. Right now, every transaction requires your approval. The roadmap will allow you to set pre-approved spending thresholds and merchant-level permissions. This means you will be able to configure an agent to spend up to a certain amount at specific merchant categories without requiring a manual approval each time.

For recurring purchases like SaaS subscriptions or regular supply reorders, this will remove the friction of the approval step while keeping you in control of the parameters. You set the rules once, and the agent operates within them.

Support for next-generation payment protocols and digital currencies

Stripe has signaled that the Link agent wallet will eventually support next-generation payment protocols and digital currencies. This aligns with Stripe's broader work in crypto infrastructure, including stablecoin issuing and card infrastructure, which was also part of the Sessions 2026 announcements. For agents operating in global or crypto-native contexts, this will expand the range of transactions they can execute.

Saved buying preferences

A feature on the roadmap will allow agents to access your purchase history to make smarter, more personalized decisions. If an agent knows you always book aisle seats, prefer a specific hotel chain, or consistently choose a particular software tier, it can surface better options without you having to specify preferences each time. This moves the agent from a transaction executor to something closer to a genuine purchasing assistant.

Global availability

The current US-only limitation is a practical constraint, not a strategic one. Global availability is planned, and given Stripe's existing international infrastructure, the rollout is likely to be relatively fast once the product is out of its initial launch phase. For founders building products with international users, this is worth tracking.

Agentic commerce as a core strategic pillar

Perhaps the most important signal from Sessions 2026 is not any single feature but the framing. Stripe explicitly positioned building economic infrastructure for AI as one of its three core strategic directions. That is not the language of a company experimenting with a side project. It is the language of a company that has decided this is where a significant portion of future commerce will happen and is building accordingly.

For founders and marketers, that signal matters. The companies that understand and build on this infrastructure early will have advantages that are difficult to replicate once the market matures. The same way that early Stripe adopters had a meaningful edge in online payments a decade ago, early adopters of agentic commerce infrastructure are likely to have a similar edge in the next wave.

Frequently Asked Questions

How does Stripe Link work?

Stripe Link is an accelerated checkout network. You save your payment details once, and those details become available at any merchant that accepts Link. At checkout, Link autofills your card information so you do not need to type it again. The agent wallet extends this by letting AI agents initiate purchases on your behalf using one-time virtual cards, while your real credentials stay inside the Link system and are never shared with the agent or the merchant.

How does Stripe Link work specifically for AI agents?

When an AI agent is connected to Link, it can initiate a purchase request on your behalf. The agent does not receive your card number. Instead, Link generates a one-time virtual card for that specific transaction. You receive a notification in the Link app showing the agent name, merchant, and amount. You approve or decline. If you approve, the transaction completes. The agent never handles your real payment credentials at any point in this flow.

How do users first encounter Stripe Link?

Most buyers first encounter Link at checkout on a Stripe-powered merchant site. After completing a purchase, Link may offer to save your payment details for faster checkout elsewhere. If you opt in, your card is stored in Link and becomes available across the Link network. For the agent wallet specifically, users typically encounter it when an AI agent they are using prompts them to connect a payment method, directing them to authenticate through the Link app.

Does Stripe Link work with ChatGPT or Perplexity?

Stripe publishes open protocols, including the skill.md file format and the Agentic Commerce Protocol, that any AI platform can implement. An agent running inside ChatGPT or another AI platform can interact with Link if the platform has implemented the protocol. Whether specific platforms like Perplexity have formally integrated the Link agent wallet is not publicly confirmed at the time of writing, but the technical pathway is open to any platform that chooses to implement it.

What is the difference between Link autofill and the Link agent wallet?

Link autofill is the standard checkout acceleration feature. It fills in your saved payment details when you are checking out on a merchant site yourself. The Link agent wallet is a separate capability that lets an AI agent initiate purchases on your behalf, with your approval, using virtual cards rather than your real credentials. Autofill is for human-initiated checkouts. The agent wallet is for agent-initiated purchases.

Is the Link agent wallet available outside the US?

At launch, the Link agent wallet is available in the US only. Global availability is on the roadmap. You can join the waitlist at link.com/in/agents regardless of your location to be notified when access expands.

Can I set spending limits for my AI agent?

At launch, every transaction requires your explicit approval in the Link app. Granular controls that let you set spending thresholds and pre-approved merchant categories are on the roadmap but not yet available. When that feature ships, you will be able to configure an agent to spend within defined parameters without requiring approval for each individual transaction.

What agent frameworks does the Link agent wallet support?

The Link agent wallet works with Claude, OpenClaw, and custom-built agents. The open implementation is available on GitHub for developers building with other frameworks. Stripe's Agentic Commerce Protocol is designed to be framework-agnostic, so any agent that implements the protocol can interact with Link.

Putting It All Together

The Link agent wallet is a well-designed product that solves a real problem: how do you let AI agents complete purchases on your behalf without creating security risks or losing control of your spending?

Stripe's answer is a combination of credential isolation, explicit approval flows, one-time-use virtual cards, and a full audit trail. The result is a system where agents can be genuinely useful in commerce workflows without requiring you to hand over your financial credentials or trust that the agent will always make the right call.

For founders, the immediate opportunity is to understand where agent-driven purchases fit into your product or your customers' workflows. For marketers, it is worth thinking about how in-context shopping changes the discovery and conversion funnel. For platform operators, the private preview waitlist is the right next step.

The broader shift here is that payments infrastructure is becoming programmable in a new way. Not just through APIs that developers call, but through protocols that AI agents understand natively. Stripe is building that layer, and the Link agent wallet is the first consumer-facing piece of it.

If you want to understand how your content and messaging need to evolve as AI agents become a meaningful part of the buyer journey, TryReadable's analysis tools can help you evaluate how your current content performs in AI-mediated contexts. And if you are curious about how other brands are navigating this shift, the TryReadable brands library has examples worth exploring.

The infrastructure for agentic commerce is being built right now. The founders and marketers who engage with it early will be better positioned than those who wait for it to become obvious.

Sources referenced in this article: Stripe Sessions 2026 announcements, Link agent wallet, Stripe agentic commerce documentation, Enable in-context shopping on AI agents.

Sources

- Everything we announced at Sessions 2026

- Give your agent a wallet you control.

- Agentic commerce | Stripe Documentation

- Enable in-context shopping on AI agents | Stripe Documentation

- Google Search Central documentation

- Google AI Overviews documentation

- OpenAI announcement archive

- Anthropic documentation

- Schema.org structured data vocabulary

- W3C JSON-LD specification

- Google Analytics developer docs

- NIST AI Risk Management Framework

How fast can your AI agents move if payment never slows them down?

We'll show you how to architect agentic workflows that handle real transactions securely, and help you decide if Link agent wallets fit your product roadmap.